IVC INTRODUCES THE 16TH EDITION OF THE STUDY "THE FIBER YEAR" WITH KEY SECTOR DATA

- Fiber Production for the first Time in five Years lower than Consumption

In a press conference on May 3rd 2016, the industry association IVC published in an established tradition both the national and the global sector data: Andreas Engelhardt, CEO of The Fiber Year GmbH left no question about all important raw materials, natural and synthetic fibers and nonwovens unanswered and presented In his study a forecast horizon till 2020. 20 country profiles of leading production as well as consuming nations completed next to statements from sector experts and an extensive statistical annex the new edition. The key messages were focused on production, consumption and trading volume.

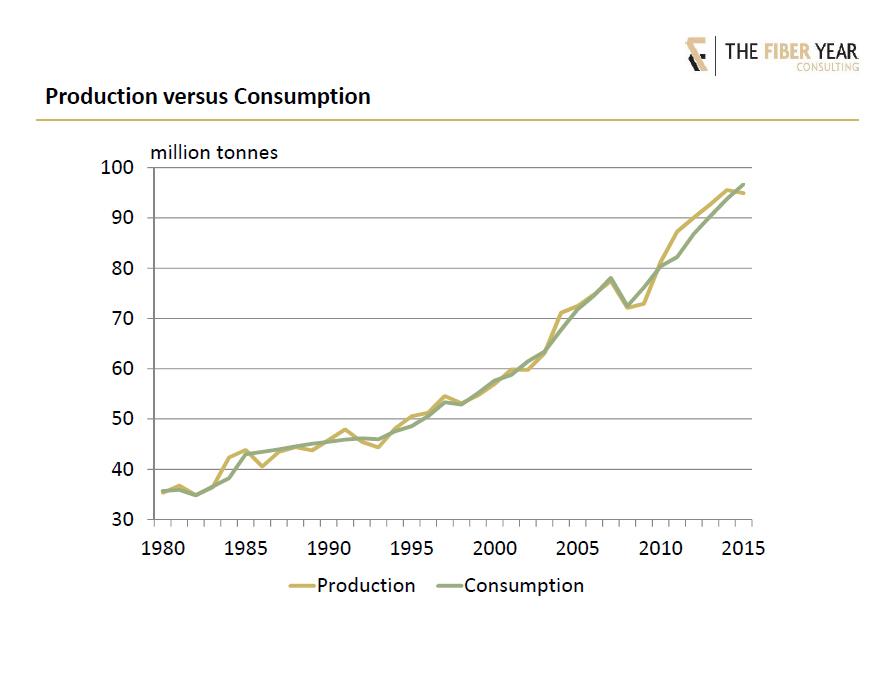

For the first time in five years fiber production is less than consumption

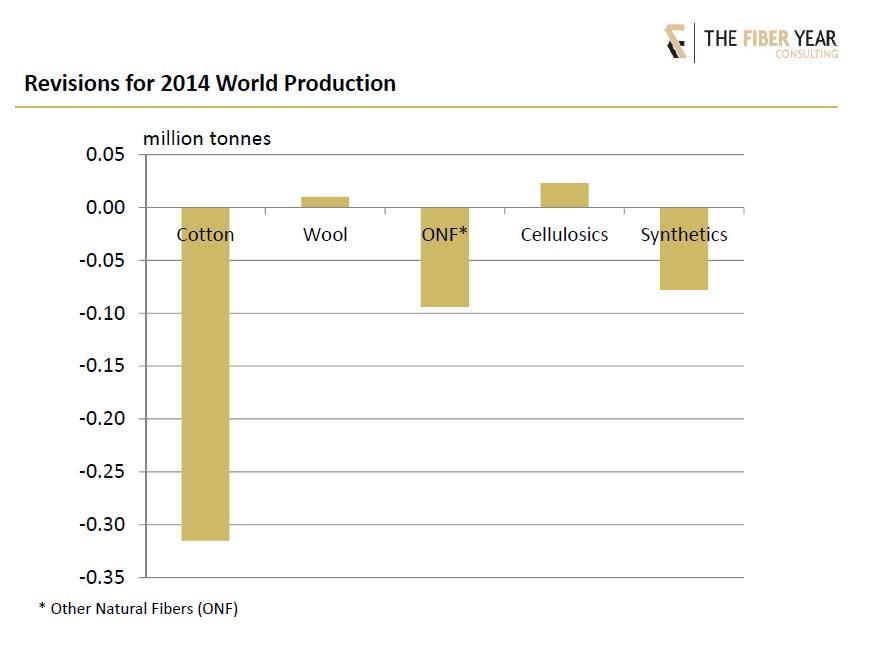

Since 2008 the global fiber production dropped again for the first time. The global volume fell by 0.7% to 94.9 million tons. The decline was decisive caused due to cotton which experienced its steepest decline in forty years. The production in the current season is estimated with 22.0 million tons, a decrease of 15.6% compared to the previous season. With a slight decrease in demand by 2.2% at the same time the stocks remain with over 20 million tons still at an enormous height. High growth rates of China's chemical fiber industry let expect a massive supply surplus. The global fiber demand in the past year has grown to 96.7 million tons. This represents an increase of 3.1% over the previous year, the weakest growth in four years due to a continuously decreasing growth of demand.

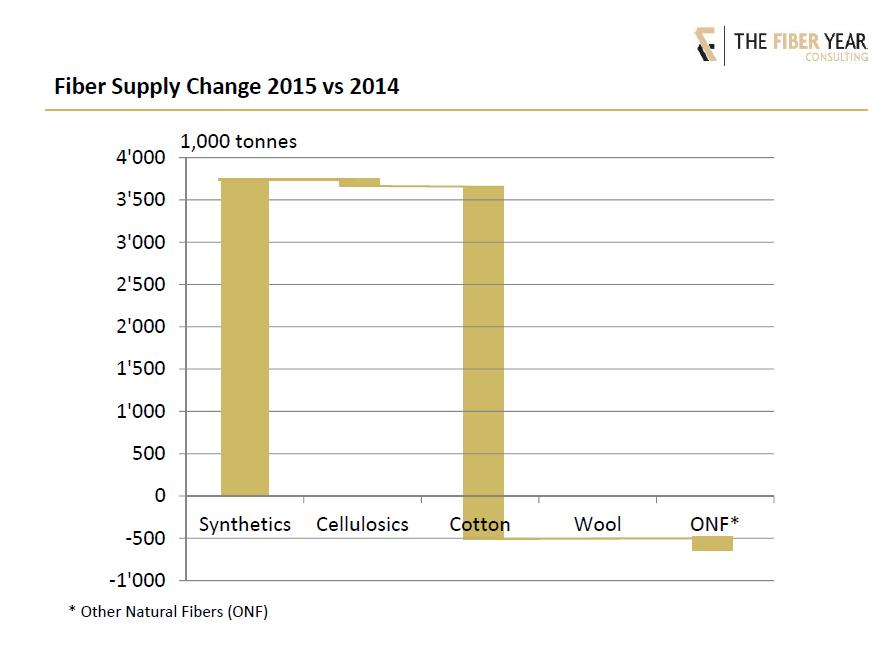

With a world population of about 7.3 billion people, this results in an average consumption per capita of 13.3 kg of textile materials for garments, home textiles, carpets and technical textiles. Synthetic fibers showed an increase of 6.6% to 60.7 million tons, significantly driven by a growth of polyester. The increase is largely caused by the area of filament yarn, as staple fibers achieved a moderate growth of 2.4% only. This can be seen as a recovery after this part of the sector showed in the last year a decline for the first time since 2008.

Cellulose fibers showed for the first time after seven years with strong growth a slight fall in production of 1.2% to 6.1 million tons. The market is almost completely dominated by staple fibers. Due to a growth across Europe and Asia viscose fibers could increase their volume by 1.1% to 4.9 million tons. In contrast Acetate showed a loss in a second consecutive year. A decreasing production activity was seen in all markets and regions with a global slump of 7.5% to 0.9 million tons. This drastic cut was significantly stronger than the losses in the end-use consumption, which can be seen as a clear indication of global destocking. The long-term shrinkage of cellulosic yarns for textile applications has developed further, so that the global supply of about 350 000 tons is equivalent to the level of the early 1930s.

The market for natural fibers experienced with a reduction of 13.2% to 28.1 million tons the biggest annual decline since 1986, which is mainly due to cotton. The production of wool was unchanged at 1.1 million tons while for bast fibers a reduction of about 5% is expected.

In a focus on the different countries, the People's Republic of China could further strengthen its dominant position with an increase in production output by 8.9% to more than 47 million tons. The United States could consolidate their second place despite a slight decline of 2.5% to 2.9 million tons, while India experienced a continued decline in the fifth following year to 2.6 million tons.

Trading volume grows unabated

According to the World Trade Organization (WTO) during the year 2014 the textile and clothing exports reached around USD 820 billion. The for the yearbook researched trade flows of 26 countries and the EU (28) estimate that the worldwide export will fall to USD 780 billion in 2015. While the Chinese exports developed a first decrease in six years, Bangladesh, Cambodia, Myanmar and Vietnam were able to continue to raise their export value. The dynamic development particular of Vietnam with its booming textile industry can be attributed to the influence of free trade agreements.

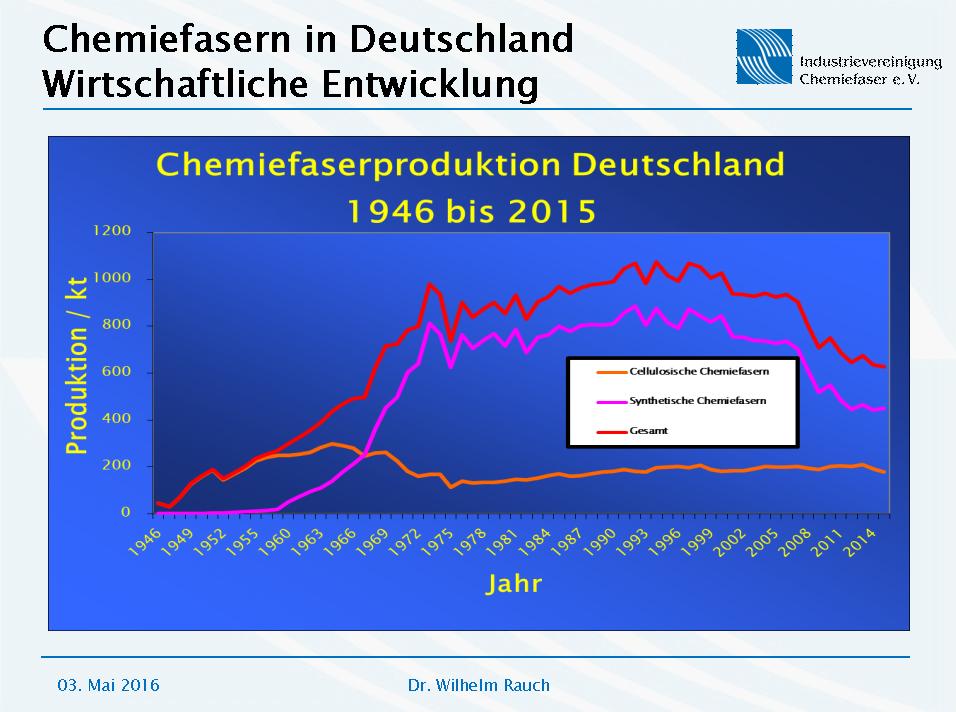

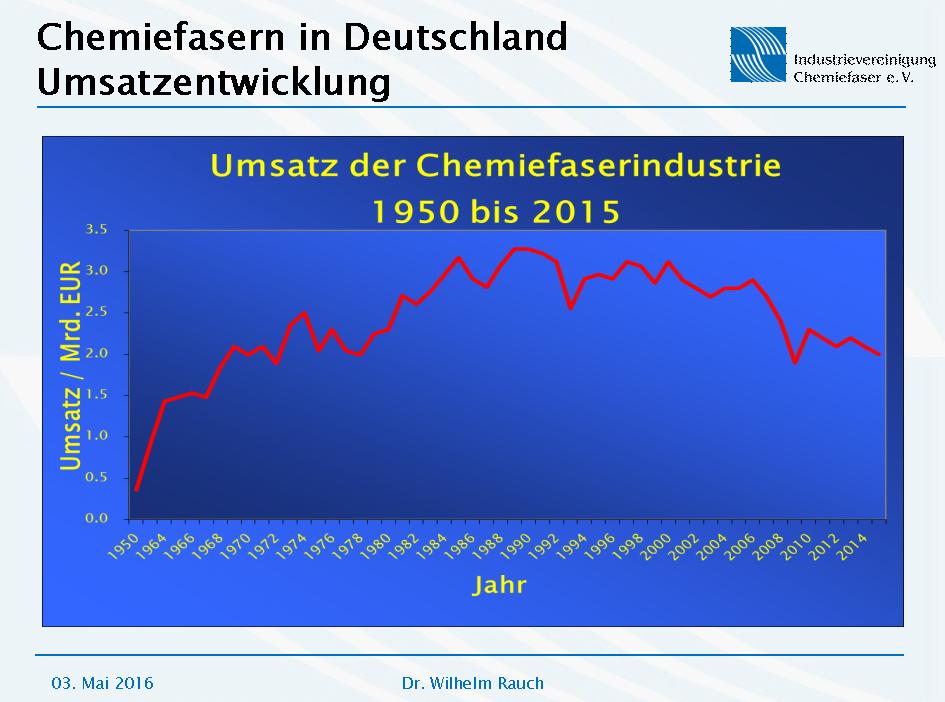

Fiber production in Germany

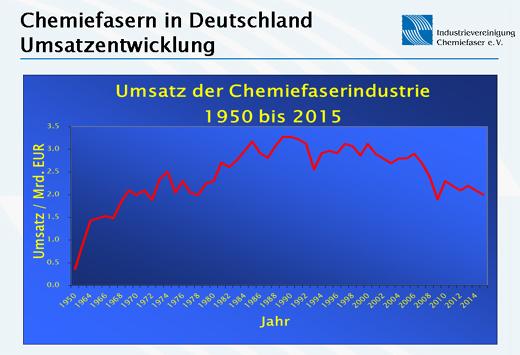

Despite international trends and many political challenges, which increasingly plague the German chemical fiber producers, man-made fibers "made in Germany" are still no dying species, Dr. Wilhelm Rauch, managing director of the industry association said.

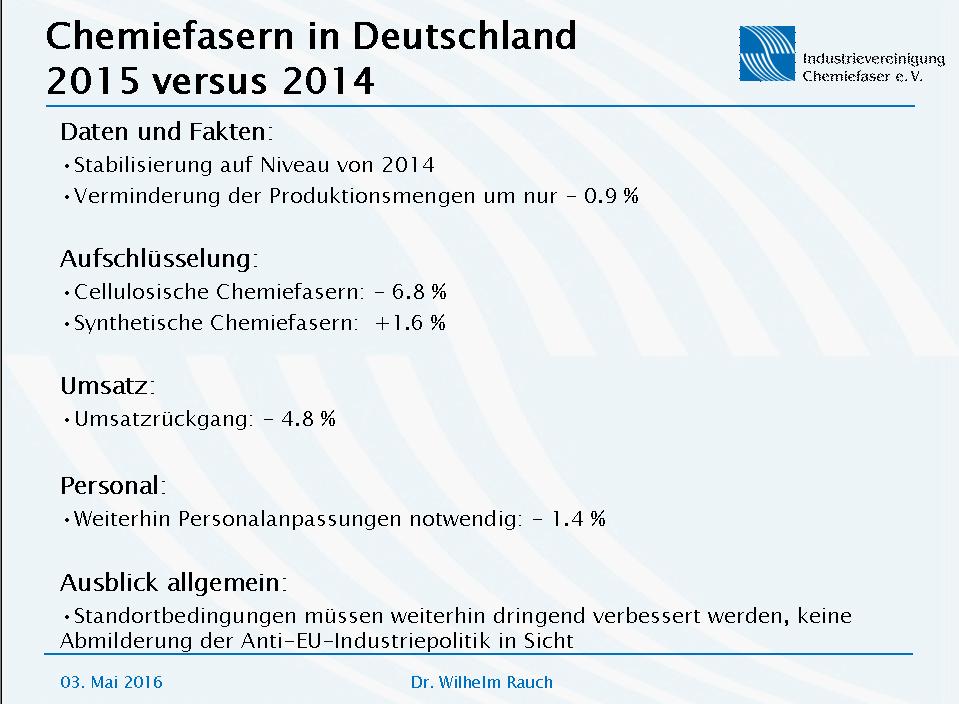

While in 2014 the chemical fiber industry in Germany suffered a decline in production volumes of 6.1%, the production volume stabilized at almost the same prior-year level. The production of cellulosic fibers remained with a reduction of - 6.8% (previous year - 8.6%) - conform to the worldwide slump of cotton. Synthetic fibers (in particular Polyester) however achieved a slight increase of + 1.6% (last year - 4.9%). Thus the reduction in production volumes kept with - 0.9% in limits.

As consequences of this a sales decline of - 4.8% and associated necessary personnel adjustments with -1.4% are alarming signals, that the site conditions for chemical fiber producers in Germany (and Europe) are urgently in a need of improvement. A positive turnaround could certainly bring a fair competition protecting and an industry-friendly approach of the EU business policy. But the emphasis of the current policy debates - about the recognition of the market economy status of China as an example of politically motivated developments let suppose a very different intension, so Mr. Rauch. Despite unfavorable economic expectant conditions it is to owe the commitment and innovation power of the local manmade fiber sector that they claim to withstand the international competition.

Nevertheless, the sector would appreciate a somewhat lower political headwind.

Fiber processing

Fiber processing

In 2015 the processing of all types of fiber in Germany could not keep the level of the previous year and suffered a decrease of -11.6%. The total imports of chemical fibers - mostly from the 28 EU countries with +54% followed by Asia with + 40% - show a plus of 1.1% (synthetic staple fibers +1.9% and filaments +1.7%), while cellulosic fibers suffered a slump of -7.4%. The total export is declining slightly (- 2.0%). Despite the reduction of total exports, here the shares in the various regions of the world compared to the previous year stood unchanged.

Further information is available at:

Andreas Engelhardt

CEO

The Fiber Year GmbH

Hauptstraße 19

9042 Speicher, Schweiz

Tel.: + 41 / 71 / 450 06 82

E-mail: Engelhardt@thefiberyear.com

Creta Gambillara

Economics and Public Relations

Industrievereinigung Chemiefaser e.V.

Mainzer Landstraße 55

60329 Frankfurt am Main

Tel.: 069 / 279971 – 39

E-mail: Gambillara@ivc-ev.de